Compare Car Insurance Rates

Instantly compare car insurance quotes to find the cheapest rate.

Why comparing auto insurance quotes is important

You’re looking to save money on car insurance, and you know you have to comparison shop to find the best deal.

However, many auto insurance quote comparison websites can’t sell you insurance. Instead, they make money by selling your personal information to insurance companies and brokers.

When you let Gabi do the comparison shopping for you, we handle everything. Like a true concierge service, we’ll find the best price, contact the insurance company, and get your policy set up.

How to compare car insurance quotes

You need an auto insurance policy that covers your needs (without going overboard) and doesn’t cost an arm and a leg. Take these steps to make sure you’re getting the best deal:

- Year

- Make

- Model

- Special features

- Safety features

Liability: Covers the other drivers on the road and meets most state’s legal requirements, but won’t protect you if you’re involved in an accident.

Collision: Provides protection against road accidents. If you’re involved in an accident, your insurer will cover all or part of the cost of repairing or replacing your vehicle, depending on your coverage limits.

Comprehensive: Protects you against practically everything else that can happen to your car. That includes damage from natural disasters, vandalism, and theft.

Full coverage is great to have, especially for drivers who frequently park on busy streets, but not everyone needs it. If your car is an older model, typically parked in a garage, or not driven heavily, you may save money by cutting down on insurance.

Not sure what you need? The licensed insurance agents at Gabi can help you choose the perfect coverage level for you!

You can compare policies by contacting insurance providers directly. For an easier way, use Gabi to compare multiple auto insurance rates and policies from nationwide providers in just a few minutes (or less).

Comparing auto insurance rates can save you money

Gabi takes the effort out of comparison shopping by letting you link your current insurance account. We can automatically analyze your policy to determine information about your coverage, car, and the drivers on your policy.

We can then look for a better rate—with equal or better coverage—from other insurance companies. Within a few minutes, we’ll let you know if you’ve got the best deal, or if you can save money by switching.

Unlike some car insurance comparison tools, we also offer renters and home insurance quote comparisons. Using these, you can determine whether you’ll save money by bundling your auto and home insurance, or if you can save the most by using two companies.

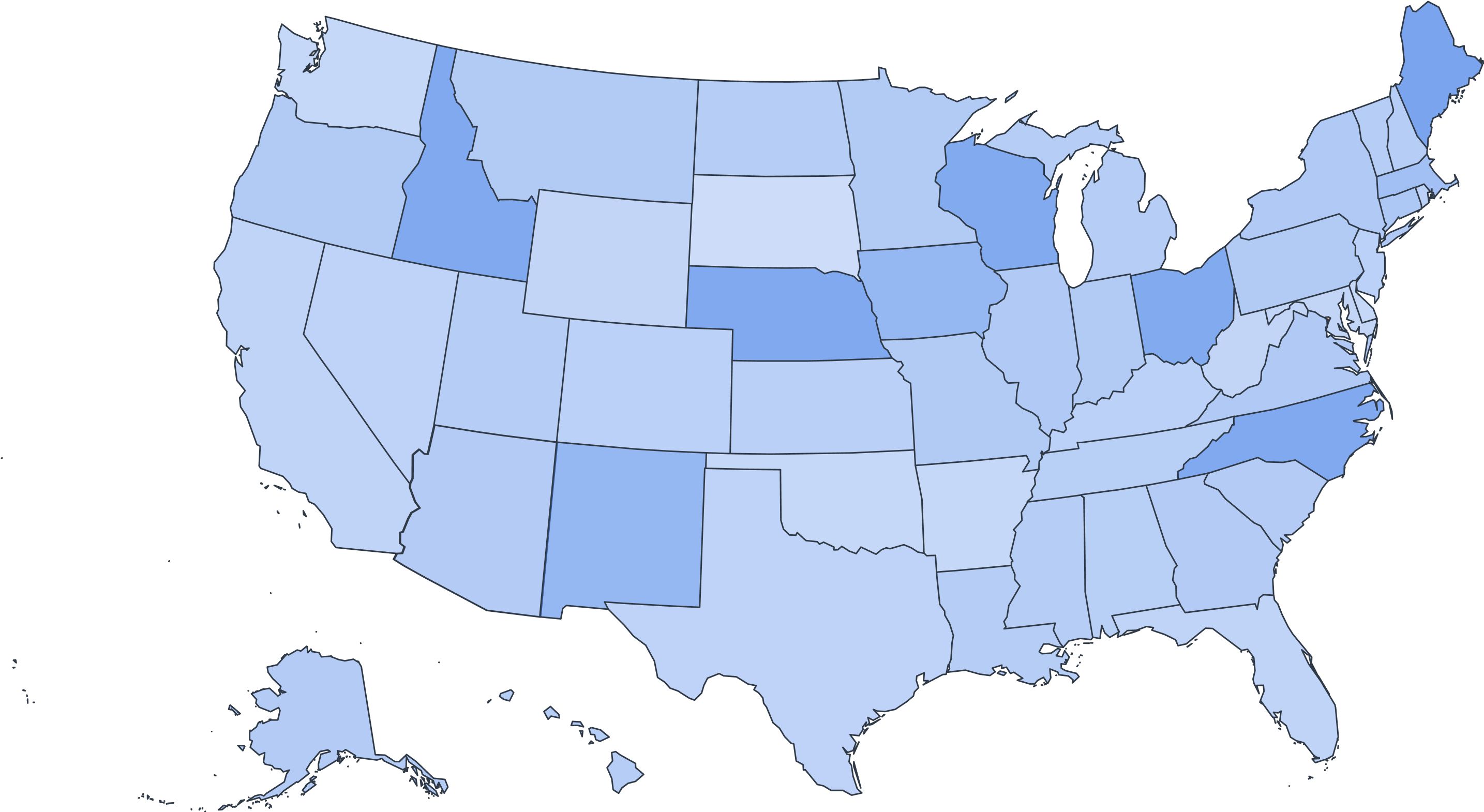

Can you save money by switching?

Many people are overpaying for their insurance and don’t realize it because they haven’t looked for a better deal. You can keep your same car, driving habits, record, and coverage, and still save money simply by switching insurance providers.

We’ve analyzed how much Gabi users could save to figure out the average overpayment from drivers in every state.

Average Monthly Car Insurance Overpayment By State

See why customers love Gabi.⊛

What impacts your car insurance rates?

The insurance provider you choose is important, however these are the factors that affect your car insurance rates.

Car Insurance Comparison by Age and Gender

Your age can be a major factor in how much you pay, as young drivers tend to be riskier drivers. Gender can play a role as well, although it’s not as important of a factor.

Auto Insurance Rates by Age

Average Auto Insurance Rates for People Under 20

| Company | Average Annual Premium |

|---|---|

| Allstate | $1,780 |

| Clearcover | $2,890 |

| Mercury | $2,498 |

| MetLife | $2,351 |

| National General | $2,505 |

| Progressive | $2,877 |

| Travelers | $2,298 |

Average Auto Insurance Rates for Those in Their 20’s

| Company | Average Annual Premium |

|---|---|

| Allstate | $1,943 |

| Bristol West | $2,514 |

| Clearcover | $1,877 |

| Mercury | $2,159 |

| MetLife | $1,692 |

| National General | $1,979 |

| Nationwide | $1,754 |

| Progressive | $1,891 |

| Travelers | $2,230 |

Average Auto Insurance Rates for Those in Their 30’s

| Company | Average Annual Premium |

|---|---|

| Allstate | $2,084 |

| Bristol West | $2,318 |

| Clearcover | $1,740 |

| Mercury | $2,173 |

| MetLife | $1,663 |

| National General | $1,960 |

| Nationwide | $1,867 |

| Progressive | $1,693 |

| Travelers | $1,958 |

Average Auto Insurance Rates for Those in Their 40’s

| Company | Average Annual Premium |

|---|---|

| Allstate | $2,495 |

| Bristol West | $2,597 |

| Clearcover | $2,049 |

| Mercury | $2,309 |

| MetLife | $1,909 |

| National General | $2,112 |

| Nationwide | $2,211 |

| Progressive | $2,058 |

| Travelers | $2,300 |

Average Auto Insurance Rates for Those in Their 50’s

| Company | Average Annual Premium |

|---|---|

| Allstate | $2,581 |

| Bristol West | $2,023 |

| Clearcover | $1,901 |

| Mercury | $1,663 |

| MetLife | $2,218 |

| National General | $1,862 |

| Nationwide | $2,179 |

| Progressive | $2,041 |

| Travelers | $2,429 |

Average Auto Insurance Rates for Those in Their 60’s

| Company | Average Annual Premium |

|---|---|

| Allstate | $2,347 |

| Bristol West | $2,089 |

| Clearcover | $1,665 |

| Mercury | $1,456 |

| MetLife | $1,590 |

| National General | $1,790 |

| Nationwide | $1,727 |

| Progressive | $1,563 |

| Travelers | $1,973 |

Average Auto Insurance Rates for Those Over 70+

| Company | Average Annual Premium |

|---|---|

| Allstate | $2,198 |

| Bristol West | $2,940 |

| Clearcover | $1,588 |

| Mercury | $1,708 |

| MetLife | $1,720 |

| National General | $2,265 |

| Nationwide | $1,726 |

| Progressive | $1,428 |

| Travelers | $1,827 |

Auto Insurance Rates by Gender

| Gender | Average Yearly Premium |

|---|---|

| Female | $1,930 |

| Male | $1,951 |

Compare Auto Insurance Rates By Driving History

Your driving record is also important. The more recent accidents or traffic violations you’ve had, the more you’ll wind up paying.

Average Annual Premium

| Number of Incidents | Average Annual Premium |

|---|---|

| 0 | $1,416 |

| 1 | $1,604 |

| 2 | $1,883 |

| 3 | $2,126 |

| 4 | $2,337 |

| 5 | $2,493 |

| 6 | $2,711 |

| 7 | $2,985 |

| 8 | $3,061 |

| 9 | $3,158 |

| 10 | $3,174 |

| 11 | $3,208 |

| 12 | $3,666 |

Auto Insurance Premiums by Coverage Type

Your coverage limits, types, and deductibles will directly impact your premiums. You’ll have to decide whether you prefer more coverage and lower deductibles, or a lower cost.

Average Car Insurance Premiums by State Full vs Non Full Coverage

| State | Average Annual Premium (Non Full Coverage) | Average Annual Premium (Full Coverage) |

|---|---|---|

| Alabama | $916 | $1,939 |

| Alaska | NA | NA |

| Arizona | $953 | $1,901 |

| Arkansas | $1,175 | $1,922 |

| California | $964 | $2,249 |

| Colorado | $1,022 | $2,193 |

| Connecticut | $1,764 | $2,225 |

| Delaware | $3,611 | $2,282 |

| District of Columbia | $1,087 | $2,020 |

| Florida | $1,508 | $2,568 |

| Georgia | $1,628 | $2,688 |

| Hawaii | $547 | $682 |

| Idaho | $761 | $1,178 |

| Illinois | $803 | $1,517 |

| Indiana | $845 | $1,563 |

| Iowa | $732 | $1,479 |

| Kansas | $753 | $1,989 |

| Kentucky | $1,407 | $2,288 |

| Louisiana | $1,688 | $2,971 |

| Maine | $697 | $1,147 |

| Maryland | $1,768 | $2,556 |

| Massachusetts | $1,625 | $1,829 |

| Michigan | $1,779 | $2,704 |

| Minnesota | $1,101 | $1,578 |

| Mississippi | $944 | $2,050 |

| Missouri | $1,263 | $1,929 |

| Montana | $746 | $1,749 |

| Nebraska | $920 | $1,672 |

| Nevada | $1,271 | $2,297 |

| New Hampshire | $933 | $1,249 |

| New Jersey | $1,675 | $2,470 |

| New Mexico | $858 | $1,747 |

| New York | $2,157 | $2,607 |

| North Carolina | $989 | $1,534 |

| North Dakota | $1,180 | $1,978 |

| Ohio | $789 | $1,450 |

| Oklahoma | $859 | $1,827 |

| Oregon | $1,187 | $1,784 |

| Pennsylvania | $1,066 | $1,812 |

| Rhode Island | $1,872 | $2,589 |

| South Carolina | $1,611 | $2,191 |

| South Dakota | $810 | $1,612 |

| Tennessee | $832 | $1,833 |

| Texas | $1,134 | $2,244 |

| Utah | $1,329 | $1,741 |

| Vermont | $694 | $1,331 |

| Virginia | $1,043 | $1,681 |

| Washington | $1,178 | $1,994 |

| West Virginia | $856 | $1,912 |

| Wisconsin | $737 | $1,418 |

| Wyoming | $735 | $1,521 |

Average Car Insurance Premiums by Insurance Company Full vs Non Full Coverage

| Carrier Name | Average Annual Premium (Non Full Coverage) | Average Annual Premium (Full Coverage) |

|---|---|---|

| Allstate | $1,123 | $2,341 |

| Bristol West | $1,444 | $3,040 |

| Clearcover | $1,099 | $1,985 |

| Mercury | $1,138 | $2,296 |

| MetLife | $712 | $1,890 |

| National General | $1,216 | $2,413 |

| Nationwide | $1,086 | $2,061 |

| Progressive | $1,396 | $2,198 |

| Travelers | $1,396 | $2,198 |

Remember, full coverage insurance includes the three main types of car insurance: liability, collision, and comprehensive. The liability portion covers other drivers (and their property) in the event of an accident. The collision coverage protects you and your property in an accident. Comprehensive coverage protects your vehicle against vandalism, damage from non-accidents, and theft.

The right amount of car insurance for you depends on the make and model of your car, how (and where) you drive, and your unique needs.

Compare Insurance Rates by Your Location

Your location can also impact your rates, as theft, vandalism, and accident frequency can vary by geographic region.

| State | Average Annual Premium |

|---|---|

| Alabama | $1,740 |

| Alaska | NA |

| Arizona | $1,705 |

| Arkansas | $1,747 |

| California | $1,987 |

| Colorado | $1,893 |

| Connecticut | $2,150 |

| Delaware | $2,468 |

| District of Columbia | $1,938 |

| Florida | $2,383 |

| Georgia | $2,474 |

| Hawaii | $615 |

| Idaho | $1,070 |

| Illinois | $1,404 |

| Indiana | $1,439 |

| Iowa | $1,385 |

| Kansas | $1,638 |

| Kentucky | $1,963 |

| Louisiana | $2,588 |

| Maine | $1,088 |

| Maryland | $2,426 |

| Massachusetts | $1,804 |

| Michigan | $2,461 |

| Minnesota | $1,465 |

| Mississippi | $1,903 |

| Missouri | $1,784 |

| Montana | $1,584 |

| Nebraska | $1,505 |

| Nevada | $2,112 |

| New Hampshire | $1,222 |

| New Jersey | $2,365 |

| New Mexico | $1,537 |

| New York | $2,535 |

| North Carolina | $1,471 |

| North Dakota | $1,679 |

| Ohio | $1,348 |

| Oklahoma | $1,570 |

| Oregon | $1,616 |

| Pennsylvania | $1,698 |

| Rhode Island | $2,419 |

| South Carolina | $2,103 |

| South Dakota | $1,434 |

| Tennessee | $1,582 |

| Texas | $2,076 |

| Utah | $1,641 |

| Vermont | $1,279 |

| Virginia | $1,589 |

| Washington | $1,863 |

| West Virginia | $1,772 |

| Wisconsin | $1,312 |

| Wyoming | $1,400 |

Auto Insurance Costs by Vehicle Type

Luxury cars can be more expensive to repair and replace, and they tend to cost more to insure than a run-of-the-mill vehicle. Additionally, you may receive a discount for having a car with built-in safety features or anti-theft devices.

Car Insurance Comparison by Credit Score

In most states, having a poor credit history can lead to higher home and auto insurance rates.

While each of these factors can play a role in determining your premiums, insurance providers may place a different amount of importance on each factor. That’s one reason your rates can vary from one company to another, even when you’re purchasing the same amount of coverage.

3 Ways to Lower Your Car Insurance Rates

Whether you want to use Gabi to see if you’re overpaying or stick with your current insurance, here are three ways you might be able to lower your rate:

Your rates can also change over time, and making a habit of looking for quotes once or twice a year can also help you save.

If you’d prefer a hands-off approach, start comparing your auto insurance rates with Gabi and find out how much you could be saving. Even if we can’t find you a better deal today, we’ll continue to compare auto insurance rates and let you know when a cheaper policy is available.

Cheapest and Most Expensive Cars to Insure

Pricing set by insurance companies is determined by a wide variety of factors. Here are the most important ones:

Car Insurance FAQs

Same-sex married couples are also eligible to receive the discount, but it may vary by the company and state.

- USAA

- Geico

- State Farm

- Root

- Progressive

- American Family

- Farmers

- Nationwide

- AllState

If you have a question and want to talk to us over the phone, you can. Or, you can go through the entire car insurance comparison and purchase process using the online app, email, or text.

Average car insurance premiums: Gabi uses internally compiled data of customers who’ve signed up through 2020 to determine averages and drive data points. Internal data represents Gabi customers nationwide and may not reflect all available customers in the national marketplace.

Where available, Gabi sources additional data from accredited sources like the Insurance Information Institute and the National Center for Highway Safety to inform data.

All content is reviewed by a licensed insurance agent. It is intended for informational purposes only and should not be considered legal or financial advice.

Jessie Jordan

Jessie Jordan Robbie Boddy

Robbie Boddy